Yes, your renters insurance typically covers sudden and accidental water damage from burst pipes, appliance malfunctions, and plumbing failures. However, standard policies exclude gradual leaks, negligence, flooding, and sewer backups. Your personal belongings are protected, not the building structure. Report incidents immediately and document with photos and videos. You'll need separate coverage for flood damage. Understanding your specific policy limitations can save you from unexpected out-of-pocket expenses.

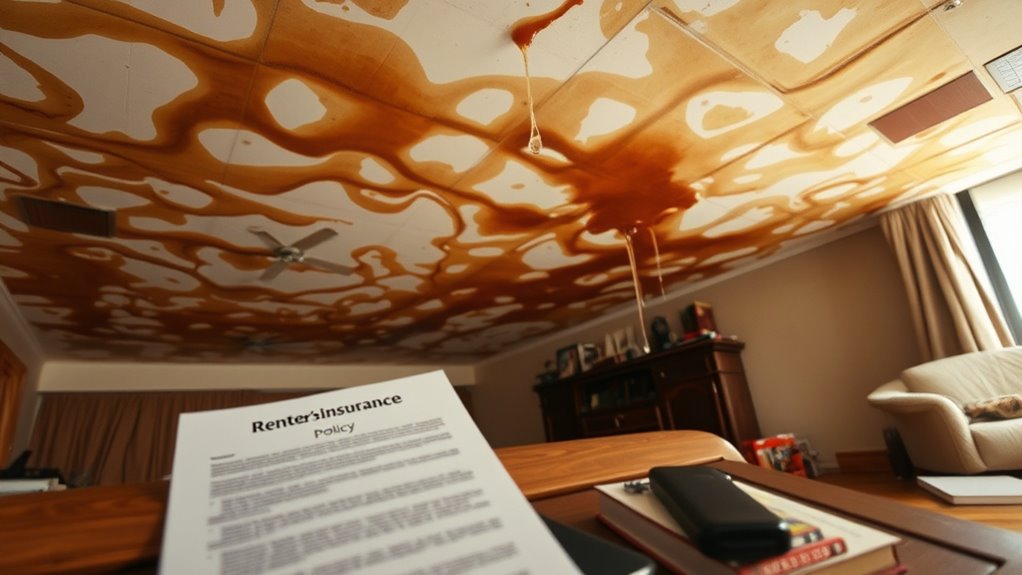

Understanding Water Damage Coverage in Renters Insurance

While many renters focus on coverage for theft or fire damage, water-related incidents actually represent one of the most common claims filed under renters insurance policies.

Your policy typically covers sudden and accidental water damage from burst pipes, appliance malfunctions, and plumbing failures. Insurance terms differentiate between covered perils and exclusions—an significant distinction when dealing with a water leak situation. If your claim is rejected, you might receive an access denied notification through your insurer's online portal.

Sudden water incidents fall under coverage, while gradual damage doesn't—a crucial distinction when pipes fail unexpectedly.

Coverage extends to accidental overflows from toilets, bathtubs, or washing machines, plus damage from ice or snow accumulation in some cases. Storm-related damage to your belongings caused by a sudden event, like a hole in the roof, would also typically be covered. It's worth noting that damage caused by frozen pipes that burst is typically included in standard renters insurance coverage.

However, your policy won't cover gradual damage from unreported leaks, wear and tear, or neglected maintenance issues. External flooding, sewer backups, and structural damage to walls generally require supplemental coverage options.

To maintain protection, you must promptly report leaks and take reasonable preventive measures to minimize damage.

Types of Water Leaks Typically Covered

Renters insurance typically covers several categories of water leak damage, provided they meet the "sudden and accidental" requirement outlined in most policies. Your coverage specifically addresses unexpected water incidents rather than gradual deterioration or negligence. Your policy may also include coverage for temporary housing costs if the water damage makes your apartment uninhabitable. It's important to document all water damage with photos and videos to support your claim when filing with your insurance company. Remember that claims resulting from water damage may be denied if you were not residing at the premises at the time of the incident.

| Water Leak Types | Coverage Specifics |

|---|---|

| Burst/Frozen Pipes | Covered when temperature maintained adequately; includes structural plumbing failures |

| Appliance Malfunctions | Protection for washing machine, dishwasher, water heater, and refrigerator leaks |

| Fixture Incidents | Covers non-negligent toilet overflows, shower pan leaks, and accidental bathtub overflows |

Your policy also typically extends to weather-induced interior leaks from storm-damaged roofs and third-party incidents like upstairs neighbor leaks. Keep in mind that coverage applies to your personal belongings damaged in these events, not the building structure itself.

Water Damage Scenarios Not Protected by Standard Policies

Understanding what your renters insurance doesn't cover is just as vital as knowing what it does. Standard policies contain significant water damage exclusions that could leave you financially vulnerable.

Don't be caught off guard—renters policies have crucial water damage gaps that could drain your savings.

External flooding from natural disasters, including hurricanes and overflowing rivers, requires separate flood insurance through the NFIP.

- Damage resulting from tenant negligence (ignoring visible leaks or failing to report issues)

- Long-term water problems like gradual leaks, mold growth from poor ventilation, or wear-and-tear

- Sewer backups, drain overflows, and sump pump failures (unless added via endorsement)

- Water seepage through foundations or groundwater infiltration

- Structural damage to building elements owned by your landlord (walls, plumbing systems, roofing)

Toilet overflow incidents may be covered by your renters insurance as long as the damage didn't result from tenant negligence.

Claims may be denied if damage stems from delayed repairs or unreported problems, making prompt reporting of all water issues essential.

Determining Responsibility: Landlord vs. Tenant

When water damage occurs in a rental property, determining financial responsibility hinges on whether the affected items are structural elements (landlord's responsibility) or personal belongings (tenant's responsibility).

Your landlord must maintain plumbing systems, walls, and roofing while your renters insurance covers your personal possessions damaged by sudden, covered water events. California law specifically requires landlords to address water damage through prompt repairs when not caused by tenant negligence. Tenants have the legal obligation to report water-related issues immediately to prevent further damage to the property.

Water leak detectors like Kangaroo sensors can provide early warning of potential issues, helping prevent extensive damage to both the property and your belongings.

Understanding these distinct coverage boundaries prevents disputes during water emergencies and guarantees you'll know exactly who pays for what damage when leaks occur.

Understanding Coverage Boundaries

Despite the seemingly straightforward nature of water damage incidents, determining financial responsibility between landlords and tenants often creates significant confusion in rental situations. Your coverage limits and claim process will depend on the specific cause of water damage and relevant maintenance responsibilities.

- Sudden pipe bursts and appliance malfunctions typically fall under renters insurance coverage.

- External flooding requires separate flood insurance policies and is excluded from standard coverage.

- Gradual leaks and normal wear-and-tear damage are almost universally excluded.

- Tenant-caused damage through negligence (e.g., leaving tubs running) may void insurance protection.

- Mold resulting from unaddressed leaks generally requires specialized endorsements.

Understanding these boundaries helps prevent claim denials and guarantees you maintain appropriate coverage for potential water damage scenarios in your rental property. A clear lease agreement detailing water damage responsibilities can significantly reduce disputes between landlords and tenants when incidents occur.

Know your policy's specific exclusions before water incidents occur.

Who Pays For What

Determining financial responsibility for water damage in rental properties hinges on four key factors: the source of the leak, maintenance history, negligence involvement, and existing insurance coverage.

Landlord obligations cover structural and systemic issues—plumbing failures, roof leaks, and pre-existing defects fall under their insurance. They must address urgent repairs within 24-48 hours to maintain habitability standards.

Your tenant responsibilities include damage from personal negligence or appliance malfunctions. If you leave a faucet running or fail to report a visible leak, you'll likely bear repair costs. Your renters insurance covers your personal belongings but won't pay for structural repairs.

Documentation proves critical during disputes—save maintenance requests, inspection reports, and photographs.

Remember: landlords cover the building's integrity while you're responsible for damage resulting from improper use or negligence.

Structural vs. Personal

The distinction between structural and personal property forms the backbone of responsibility allocation in water damage scenarios. Understanding these boundaries helps clarify who bears financial responsibility when leaks occur and guides your claim processes accordingly.

- Structural elements (plumbing, roofs, HVAC systems) fall under your landlord's maintenance obligations and insurance coverage.

- Personal belongings damaged by sudden water leaks require your renters insurance, as landlord policies never cover tenant possessions.

- Policy exclusions often apply when tenant negligence (like leaving windows open during rain) causes damage.

- Liability shifts to you for damage resulting from misuse of fixtures or unreported maintenance issues.

- Flood damage typically falls outside standard renters insurance coverage, requiring separate policies.

When filing claims, document the source of water damage to determine whether it's a landlord structural issue or a personal property claim. Prompt reporting of any water damage to your landlord is crucial, as failure to act on known leaks can invalidate your insurance claims and potentially increase your financial responsibility.

Steps to Take When Water Damage Occurs

When water damage occurs in your rental unit, you must document everything with timestamped photos, videos, and a detailed inventory of affected items before moisture compromises evidence.

You'll need to immediately prevent further damage by shutting off the main water supply, containing active leaks with towels or buckets, and moving undamaged belongings to dry areas.

Contact your landlord and insurance provider within 24-48 hours to report the incident, initiate the claims process, and coordinate professional assessment of the damage. Remember that while internal water damage from broken pipes is typically covered, you may need separate flood insurance if the water is coming from external sources like heavy rain or hurricanes.

Document Everything Immediately

Faced with the chaos of water damage, your initial priority after ensuring safety should be thorough documentation of the incident. Extensive evidence collection creates a solid foundation for your insurance claim and increases your chances of fair compensation.

- Capture wide-angle photos showing the full scope of affected areas along with close-up images of specific damage points.

- Record walkthrough videos that establish spatial relationships between damaged items and affected structures.

- Create a detailed inventory listing damaged possessions with descriptions, pre-damage condition, and replacement costs.

- Take moisture meter readings with timestamps and location tags to scientifically validate water intrusion.

- Store all digital documentation evidence in cloud storage to prevent accidental data loss.

These documentation tips transform your experience from chaotic emergency to organized evidence collection, positioning you favorably for the claims process ahead. Always contact your insurance company immediately after documenting to follow their specific instructions for the claims process and ensure timely reporting. Document any signs like peeling or bubbling paint which are clear indicators of water damage that insurance adjusters specifically look for during their assessment.

Prevent Further Damage

Once water intrusion has been detected, your immediate response directly impacts both claim outcomes and repair costs. Your initial emergency response should be shutting off the main water valve to prevent further water damage.

Turn off electricity to affected areas to eliminate shock hazards and unplug electronics near water zones.

For effective leak detection, identify specific sources such as appliance valves or pipe ruptures. Extract standing water with wet vacuums and remove saturated materials like carpets and rugs.

Deploy fans and dehumidifiers to manage environmental moisture and prevent mold growth.

For significant damage, contact professional water restoration services with IICRC certification. Place furniture on blocks and use temporary sealants for minor leaks when appropriate. Document all communications with your landlord regarding repairs to create a record of your responsible tenant behavior. Taking swift action is essential, as water damage can rapidly weaken foundations and compromise the structural integrity of the property.

Proper documentation of your mitigation efforts will demonstrate due diligence to your insurance provider.

Ensure you maintain proper ventilation in bathrooms and kitchens during cleanup to prevent additional moisture buildup that could lead to mold.

Filing a Successful Water Damage Claim

Despite the complexity of managing insurance claims, understanding the proper procedures for filing a water damage claim can greatly improve the chances of approval.

Navigating the claims process properly is key to ensuring your water damage coverage is fully realized.

Review your policy carefully to determine coverage limits for water damage, then document every aspect thoroughly with dated photos, videos, and detailed notes. Contact your insurance provider immediately after identifying damage to initiate the claim process. Working with public adjusters can provide advocacy and help secure a fair settlement for your claim. Stop the source of water damage by turning off valves to prevent additional damage and strengthen your claim.

- Secure thorough claim documentation including damage photos, repair estimates, and inventory of affected items

- Understand your policy's specific coverage limits for sudden vs. gradual water damage

- Mitigate further damage by removing standing water and drying affected areas

- Keep all receipts for emergency repairs and replacement items

- Prepare for adjuster visits by organizing evidence and creating a detailed damage timeline

Preventative Measures to Avoid Water Damage

Preventing water damage offers a more sustainable approach than managing the claim process after a disaster strikes. Implementing preventative maintenance can greatly reduce your risk exposure while protecting your belongings.

| Area | Inspection Frequency | Preventative Action |

|---|---|---|

| Appliances | Every 6 months | Replace washing machine hoses with steel-braided versions every 5 years |

| Plumbing | Monthly | Check under sinks for moisture, leaks, or corrosion |

| Drainage | Bi-annually | Clean gutters in spring/fall and confirm downspouts extend 10+ feet from foundation |

Regular plumbing inspections should include monitoring exposed pipes in unheated areas and installing water alarms near appliances. Consider smart water sensors that provide real-time alerts or automatic shutoff systems that can prevent catastrophic flooding. These detection systems require testing every six months to confirm proper functionality.

Additional Coverage Options for Complete Protection

While standard renters insurance offers baseline protection for water damage, many scenarios require supplementary coverage to guarantee thorough financial safeguards.

Don't assume basic renters insurance fully covers water damage—supplemental policies ensure complete protection.

Consider these extra coverage options to address common policy exclusions:

- Flood insurance ($100-$600 annually) protects against external flooding damage from rivers, hurricanes, and heavy rainfall.

- Water backup and sump overflow coverage ($40-$75 annually) covers sewer/drain backups and sump pump failures.

- Scheduled personal property coverage ($1-$3 monthly per $1,000) extends limits for high-value items damaged by water.

- Equipment breakdown coverage ($25-$50 annually) covers repair costs for appliances damaged by electrical/mechanical malfunctions.

- Loss of use coverage typically provides 20-30% of your personal property limit for temporary housing during water damage repairs.

Real-Life Examples of Water Leak Claims

Insurance claims for water damage reveal distinct patterns of coverage acceptance and denial in everyday rental situations.

Consider these real life examples: A tenant whose upstairs neighbor's bathtub overflowed saw claim success when their waterlogged furniture was replaced due to the sudden, accidental nature of the incident.

Likewise, when winter temperatures caused pipes to burst despite maintained heating, insurers typically covered damaged electronics and clothing.

Conversely, claims involving gradual ceiling leaks from long-ignored roof issues were denied as maintenance failures.

A washing machine malfunction that destroyed nearby belongings demonstrated high claim success rates, especially with Equipment Breakdown Coverage.

Meanwhile, sewage backups required specific endorsements for coverage, highlighting the importance of understanding your policy's inclusions and exclusions before water damage occurs.

Frequently Asked Questions

Does Renters Insurance Cover Water Damage to Neighboring Units?

Your renters insurance typically covers water damage to neighboring units through your liability coverage if you're responsible for the leak.

For example, if your overflowing bathtub or burst pipe damages a neighbor's apartment, your policy can help pay for repairs.

However, coverage won't apply for gradual leaks you've neglected, external flooding, or sewer backups.

Prompt reporting and documentation are essential when water from your unit affects neighboring property.

Can I Claim Temporary Housing Costs During Water Damage Repairs?

Yes, you can claim temporary housing costs while your rental is uninhabitable due to covered water damage.

Your policy's loss of use coverage typically provides 20-30% of your personal property limit for hotel stays, supplementary meal expenses, and other necessary costs.

The claim process requires documenting the uninhabitability and submitting itemized receipts.

Be aware that gradual leaks, maintenance issues, floods without specific endorsements, and costs exceeding normal living standards aren't covered.

How Does Previous Water Damage Affect My Premium Rates?

Previous water damage claims greatly impact your premium rates.

You'll likely face premium adjustments for 3-5 years following a claim, especially if payouts exceed $1,000. Negligence-related incidents trigger steeper increases than sudden, unavoidable events.

Multiple claims may lead to non-renewal. You can mitigate these effects by installing smart water sensors, maintaining good credit, and choosing higher deductibles.

State regulations vary, with some prohibiting rate hikes for initial claims in certain regions.

Will Renters Insurance Cover Leaks Caused by Pets?

Your renters insurance generally won't cover direct pet-related exclusions like water damage from chewed pipes or scratched fixtures.

However, you're typically protected if your pet accidentally causes sudden water damage to others' property through covered perils (like knocking over a washing machine).

Be aware of coverage limits for liability claims if your pet's actions damage neighboring units.

Gradual damage and intentional destruction are specifically excluded, so report any incidents promptly.

Can Multiple Roommates File Separate Claims for Water Damage?

Yes, you can file separate claims for water damage if you and your roommates maintain individual renters insurance policies.

This approach avoids shared claim limits and prevents premium increases affecting everyone.

However, with a joint policy, you'll need all policyholders' endorsements on claim checks and must divide payouts within policy limits.

Establish clear roommate agreements beforehand to determine responsibility for deductibles and documentation when water damage occurs.